Kelly Coughlin, CPA

AI Can Guess. But a Guess Is Not Financial Clarity

AI can do impressive things.

It can read transaction data.

It can identify patterns.

It can suggest categories.

It can flag unusual activity.

It can summarize financial information faster than a person.

That is useful.

But business owners need to be careful about what AI is actually doing.

In many cases, AI is not “understanding” your business. It is making a prediction based on data, patterns, rules, language, and probability.

Sometimes that prediction is helpful.

Sometimes it is wrong.

And in accounting, tax, and business finance, a confident guess can be dangerous.

A deposit might look like revenue.

But it could be a loan, transfer, owner contribution, reimbursement, refund, or balance sheet item.

A payment might look like a deductible business expense.

But it could be personal, capitalized, reimbursable, payroll-related, loan-related, or subject to special tax treatment.

AI can make a guess.

But a guess is not financial clarity.

That is the point business owners need to understand.

AI can help with accounting and bookkeeping. It can reduce repetitive work. It can organize data faster. It can help surface issues. It can help business owners get better financial information faster and cheaper.

But AI alone is not smart enough to provide reliable business and tax clarity.

For AI to be useful in accounting and tax, it must be trained by subject matter experts. It must be educated with accounting logic, tax rules, business context, and professional standards. And its results must be reviewed by people who understand what the information means.

Business owners do not need artificial confidence.

They need financial clarity.

That clarity comes from the right combination of transaction data, AI processing, accounting logic, CPA review, and owner confirmation.

Table of Contents

Why AI Feels So Convincing

What AI Can Actually Do With Financial Data

Where AI Starts Guessing

Why Transaction Categorization Is Harder Than It Looks

The Deposit Problem: Revenue, Loan, Transfer, or Something Else?

The Payment Problem: Deductible, Personal, Capitalized, or Reimbursable?

Why Speed Is Not the Same as Accuracy

Why Clean-Looking Reports Can Still Be Wrong

The Risk of Artificial Confidence

Why AI Needs Accounting Logic and Tax Rules

Why AI Still Needs CPA Review

Why Owner Context Still Matters

The Better Model: AI Processing + CPA Judgment + Owner Confirmation

Where iPacio Fits

What Business Owners Should Do Next

FAQ

Why AI Feels So Convincing

AI often feels convincing because it gives answers quickly and confidently.

That is part of its appeal.

A business owner can ask a question and receive an answer in seconds. The answer may be neatly organized. It may sound professional. It may use accounting language. It may produce a summary, table, explanation, or recommendation.

That can feel like expertise.

But confidence is not the same as correctness.

A fast answer may still be incomplete.

A polished report may still be based on bad assumptions.

A clean category may still be wrong.

A summary may still miss the most important tax or business issue.

This is especially true in accounting because accounting is not just about recognizing words or patterns. It is about understanding facts, context, rules, purpose, and consequences.

AI may see a payment to Home Depot and guess “supplies.”

That might be right.

But it might be materials for a client job, equipment, a repair, a personal purchase, a capital improvement, or something connected to a specific property.

AI may see a deposit from a bank and guess “income.”

But it might be a transfer from savings, a loan advance, an owner contribution, or reimbursement from a customer.

AI may be helpful. But helpful is not the same as final.

The business owner should not confuse the appearance of certainty with actual financial clarity.

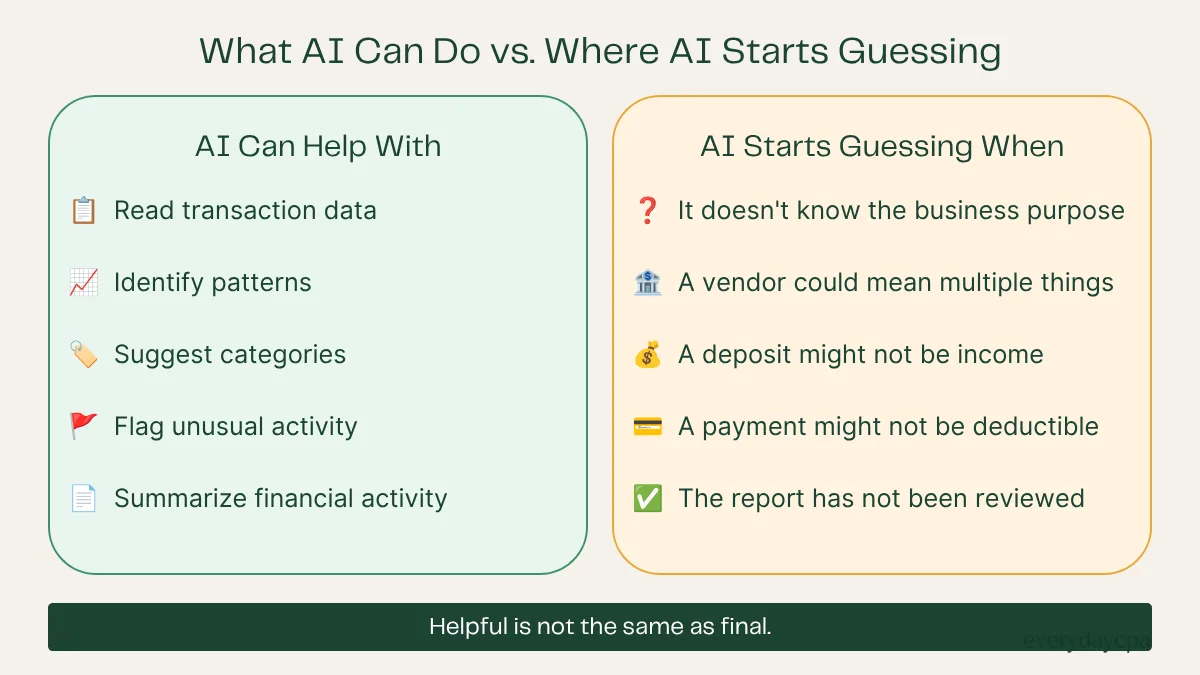

What AI Can Actually Do With Financial Data

AI can be useful in business finance because it is good at processing information.

It can review large amounts of data faster than a person. It can look for repeated patterns. It can compare transactions. It can summarize text. It can identify unusual activity. It can help organize messy information into a more usable structure.

That has real value.

AI Can Read Transaction Data

AI can help process bank and credit card activity.

It can read dates, amounts, vendors, descriptions, memo fields, payment methods, and recurring patterns.

For business owners, this can reduce time spent manually reviewing raw transactions.

AI Can Identify Patterns

AI can identify repeated vendors, recurring subscriptions, unusual deposits, seasonal spending patterns, rising costs, or expenses that seem inconsistent with prior activity.

That can help business owners notice things they might otherwise miss.

AI Can Suggest Categories

AI can suggest whether a transaction appears to be advertising, meals, software, supplies, rent, utilities, insurance, payroll, travel, repairs, or another category.

This can speed up bookkeeping.

But it also creates risk if the suggestions are accepted without review.

AI Can Flag Unusual Activity

AI may help identify transactions that look different from the normal pattern.

That could include unexpected charges, duplicate payments, unusually large deposits, new vendors, or activity that deserves owner confirmation.

This is one area where AI can be very helpful.

The owner does not need to review every routine transaction with the same intensity if a system can help prioritize what needs attention.

AI Can Summarize Financial Activity

AI can help turn financial activity into plain-English summaries.

That matters because many business owners do not want more accounting jargon. They want to understand what happened.

What came in?

Where did the money go?

What changed?

What looks unusual?

What should I ask about?

AI can help create those summaries.

But the summary still needs to be grounded in accurate books and reviewed through an accounting and tax lens.

Where AI Starts Guessing

AI starts guessing when it sees a transaction but does not know the full business context.

That happens often.

A bank transaction may include a date, an amount, and a vendor name. But that does not always explain the business purpose.

AI may know that a vendor often sells office supplies.

But it may not know what the business owner bought.

AI may know that a payment processor deposit often relates to revenue.

But it may not know whether the deposit included refunds, fees, chargebacks, transfers, or customer reimbursements.

AI may know that a payment went to a contractor.

But it may not know whether the contractor performed client work, internal admin work, repairs, marketing, technology, or something that should be tracked differently.

AI may know that a payment was made to a bank.

But it may not know whether it was a loan payment, credit card payment, transfer, fee, interest expense, or principal payment.

AI can estimate.

It can infer.

It can suggest.

But it does not automatically know.

And when financial information affects tax returns, cash flow, profitability, and business decisions, “probably right” is not good enough.

Why Transaction Categorization Is Harder Than It Looks

Transaction categorization sounds simple.

Money came in.

Money went out.

Put it in the right bucket.

But business transactions are more complicated than they appear.

The same vendor can mean different things.

The same dollar amount can mean different things.

The same transaction description can mean different things.

The same payment method can be used for business, personal, reimbursable, capital, loan, or transfer activity.

That is why categorization is not merely a clerical task.

It requires judgment.

Example: Amazon

A payment to Amazon could be office supplies.

But it could also be equipment, software accessories, shipping supplies, client gifts, cleaning supplies, personal items, books, tools, or inventory.

If AI automatically categorizes every Amazon purchase as office supplies, the books may look organized while being wrong.

Example: Home Depot

A payment to Home Depot could be supplies.

But for a contractor, it may be job materials.

For a landlord, it may be a property repair.

For a business owner, it could be a capital improvement.

For another owner, it could be personal.

The vendor alone does not answer the accounting question.

Example: Venmo or PayPal

Payments through Venmo or PayPal are especially difficult because the platform is not the true business purpose.

A payment through PayPal could be software, subcontract labor, product sales, refunds, personal transfers, customer payments, or vendor payments.

If the system only sees the payment platform, it may miss the real transaction.

This is where AI must be careful.

It can help review and organize transactions, but it needs rules, context, and review.

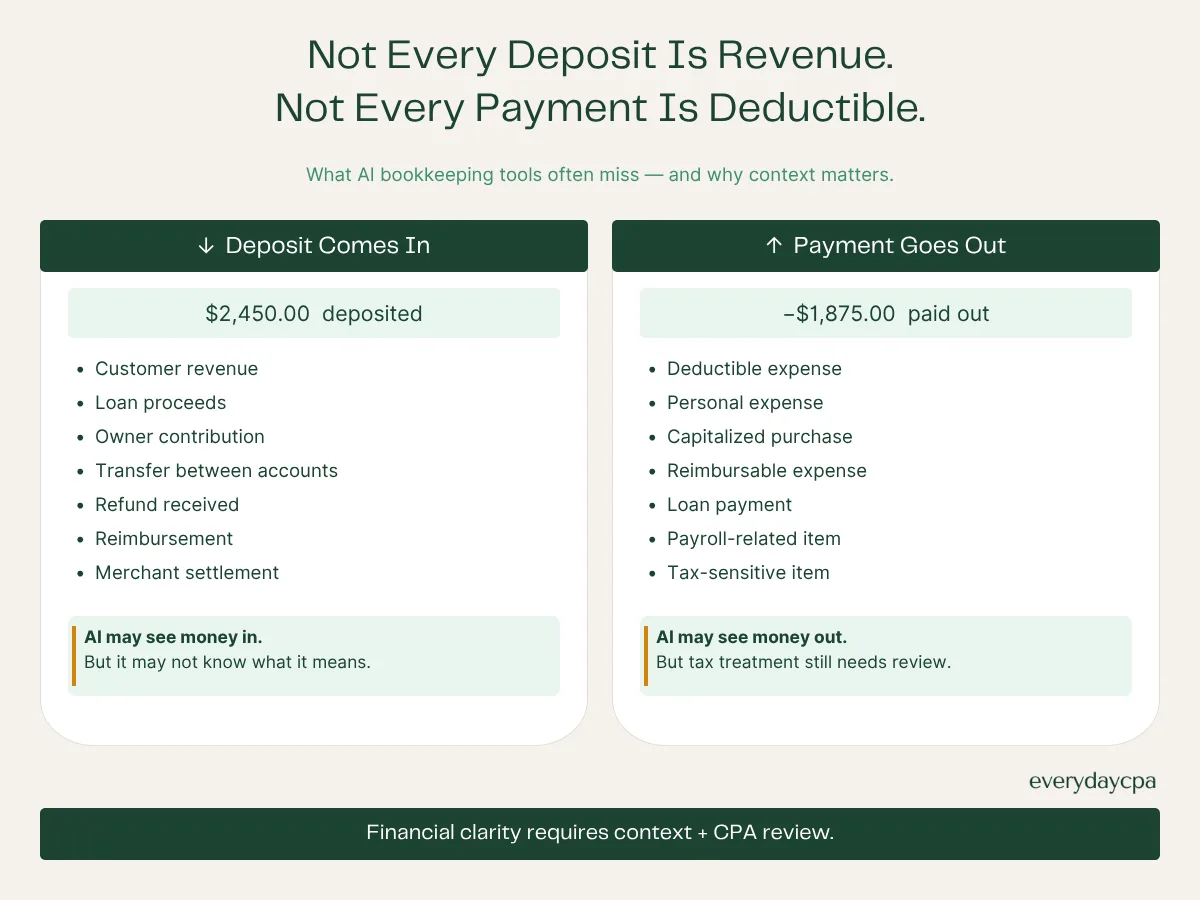

The Deposit Problem: Revenue, Loan, Transfer, or Something Else?

Deposits are one of the most important areas where AI can guess wrong.

Many business owners assume deposits are income.

Sometimes they are.

But not always.

A deposit could be:

Customer revenue

Loan proceeds

Owner contribution

Transfer from another account

Refund

Reimbursement

Insurance proceeds

Merchant settlement

Tax refund

Returned payment

Capital contribution

Personal funds accidentally deposited into a business account

If a deposit is incorrectly classified as revenue, the business may appear to have more taxable income than it actually does.

If revenue is missed because it was incorrectly treated as a transfer, income may be understated.

Both are problems.

Real-World Example

A business owner transfers $20,000 from a personal savings account into the business checking account to cover payroll during a slow month.

AI sees a $20,000 deposit.

Without context, it may suggest income.

If that amount is treated as revenue, the profit and loss report becomes wrong. Taxable income may appear higher than reality. The owner may misunderstand the business’s performance.

The transaction was real.

The deposit happened.

But the meaning was wrong.

That is why business purpose matters.

AI can see the transaction.

The owner knows the context.

The CPA knows how it should be treated.

Financial clarity requires all three.

The Payment Problem: Deductible, Personal, Capitalized, or Reimbursable?

Payments create the same problem.

A payment leaving the business bank account is not automatically a deductible expense.

It may be deductible.

But it may also be personal, capitalized, reimbursable, loan-related, payroll-related, or subject to special treatment.

Deductible Expense

Some payments are ordinary business expenses. Examples may include software, advertising, rent, utilities, supplies, insurance, and professional fees.

But even these need to be categorized correctly and documented properly.

Personal Expense

Sometimes personal spending runs through a business account by mistake.

That does not automatically make it deductible.

It needs to be identified and treated properly.

Capitalized Purchase

Some purchases may need to be treated as assets rather than current expenses.

For example, equipment, improvements, or certain larger purchases may require review.

Reimbursable Expense

Some expenses may be paid by the business but reimbursed by a customer, employee, or owner.

Those need proper handling so income and expenses are not distorted.

Loan Payment

A payment to a lender may include principal and interest.

The interest portion may be an expense. The principal portion reduces the liability. Treating the full payment as an expense can distort the financial reports.

Real-World Example

A business buys a $7,500 piece of equipment on a credit card.

AI sees the vendor and suggests “equipment expense.”

That might not be the final answer.

The purchase may need to be reviewed for capitalization, depreciation, Section 179, bonus depreciation, or other tax considerations depending on the facts.

AI can flag the transaction.

It should not make the final tax decision alone.

Why Speed Is Not the Same as Accuracy

AI is fast.

That is part of its value.

But in accounting and tax, speed is only useful if the output is reliable.

A fast wrong answer is not better than a slow correct answer.

In fact, it may be worse because it creates false confidence.

If AI quickly categorizes hundreds of transactions incorrectly, the books may appear complete. The owner may believe the work is done. The reports may be generated. The dashboard may look professional.

But the underlying information may still be wrong.

That can affect:

Profit reporting

Tax estimates

Deduction planning

Cash flow analysis

Owner compensation decisions

Loan applications

Pricing decisions

Year-end tax preparation

The point is not that AI should be slow.

The point is that AI should be supervised.

The goal is faster and better.

Not faster and wrong.

Why Clean-Looking Reports Can Still Be Wrong

One of the biggest risks of AI-assisted accounting is that the output may look clean.

A messy spreadsheet obviously looks messy.

A shoebox full of receipts obviously looks unorganized.

But an AI-generated report may look polished.

It may have headings, categories, charts, summaries, and explanations.

That can make it feel trustworthy.

But a report is only as reliable as the information and logic behind it.

A profit and loss statement can look clean and still be wrong.

A cash flow summary can look useful and still miss key timing issues.

Business owners should be careful about any financial report that looks finished but has not been reviewed.

Clean formatting is not the same as clean books.

A polished summary is not the same as financial clarity.

The Risk of Artificial Confidence

Business owners do not need artificial confidence.

They need real clarity.

Artificial confidence happens when technology makes the owner feel certain before the information has been properly reviewed.

This can happen when:

AI categorizes transactions automatically

A dashboard shows clean charts

A report summarizes activity in plain English

A tax estimate appears precise

A chatbot gives a confident answer

A bookkeeping tool says the books are complete

The danger is not that technology exists.

The danger is that the owner may stop asking questions too soon.

For example:

Are all accounts included?

Were the accounts reconciled?

Were transfers properly excluded from income and expenses?

Were owner payments handled correctly?

Were large purchases reviewed?

Were contractor payments identified?

Were tax-sensitive items flagged?

Were unusual transactions confirmed?

Were personal expenses separated?

If those questions were not answered, the confidence may be premature.

That is why AI should create better questions before it creates final answers.

Why AI Needs Accounting Logic and Tax Rules

AI becomes more useful when it is trained and structured by subject matter experts.

In accounting, that means the system needs accounting logic.

In tax, it needs tax awareness.

In business finance, it needs business context.

Accounting logic helps determine how transactions should be treated in financial records.

Tax rules help determine how those transactions may affect the tax return.

Business context helps explain what actually happened.

Professional standards help define what level of review is appropriate.

Without those guardrails, AI may simply pattern-match its way into errors.

For example, AI may learn that a certain vendor is usually categorized as meals.

But what if the payment was for an event deposit?

What if it was a client reimbursement?

What if it was a personal charge?

What if it involved entertainment rules, travel rules, or documentation issues?

Accounting logic matters.

Tax rules matter.

Context matters.

AI is only as useful as the system around it.

Why AI Still Needs CPA Review

CPA review matters because financial information has consequences.

It affects tax returns.

It affects estimated taxes.

It affects profitability.

It affects cash flow decisions.

It affects lending.

It affects owner compensation.

It affects whether the business owner understands what is actually happening.

A CPA or qualified accounting professional brings judgment to the process.

That does not mean the CPA needs to manually enter every transaction.

That is not the point.

The point is that AI can assist with compilation, but professional review is still needed to identify issues, interpret results, and apply tax and accounting knowledge.

CPA review helps answer questions like:

Does this report make sense?

Are there unusual patterns?

Are categories reasonable?

Are tax-sensitive items flagged?

Are large purchases handled properly?

Are owner payments treated correctly?

Are transfers excluded properly?

Are there missing accounts?

Are there issues the owner should understand before tax season?

This is where AI becomes powerful.

Not because it replaces the CPA.

Because it allows the CPA to spend less time on repetitive processing and more time on judgment.

Why Owner Context Still Matters

The owner still has a role in the process.

That role is not to become the bookkeeper.

The owner’s role is to provide context.

AI did not create the transaction.

The CPA did not create the transaction.

The software did not create the transaction.

The business owner created or authorized the activity.

That means the owner often knows what the transaction means.

Was the purchase for a client project?

Was the deposit a customer payment or transfer?

Was the expense personal or business?

Was the contractor doing revenue-producing work or internal admin work?

Was the payment reimbursed?

Was the transaction unusual but legitimate?

Was the charge unauthorized or fraudulent?

That context matters.

The right system should ask the owner for confirmation when needed, not force the owner to do all the accounting work.

The owner should not be buried in bookkeeping.

But the owner should stay connected to the meaning of the business activity.

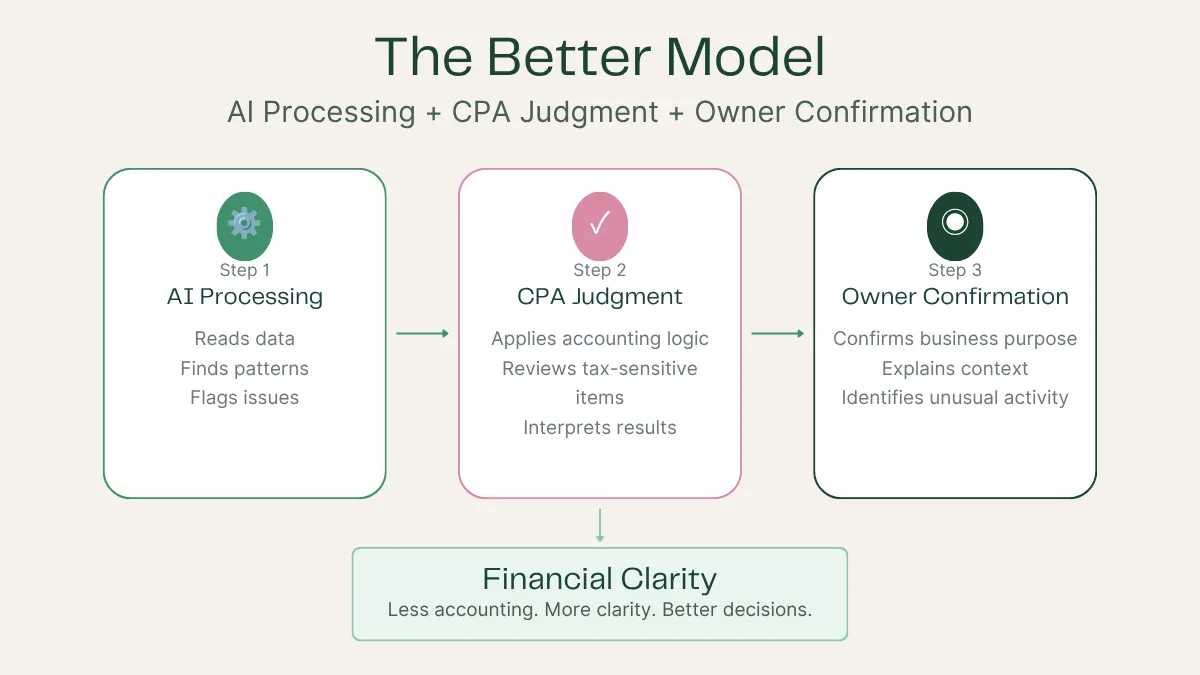

The Better Model: AI Processing + CPA Judgment + Owner Confirmation

The future of accounting should not be business owners doing everything themselves.

It should also not be AI operating alone without review.

The better model is a smarter division of labor.

AI processes information.

CPA professionals review and apply judgment.

The business owner confirms context.

Together, those pieces create financial clarity.

That model works because each part contributes something different.

AI brings speed.

The CPA brings accounting and tax knowledge.

The owner brings real-world business context.

None of those pieces is enough by itself.

AI without review can guess wrong.

CPA review without organized data can be slow and expensive.

Owner knowledge without accounting structure can remain trapped in the owner’s head.

But together, they can create better financial information faster.

That is the opportunity.

Where iPacio Fits

At EverydayCPA, we do not believe AI replaces professional judgment.

We believe AI becomes valuable when it is trained and reviewed by professionals.

That is the idea behind iPacio.

iPacio is designed to help business owners move from raw financial activity to clearer financial information without forcing the owner to become the bookkeeper.

AI can help compile the information.

EverydayCPA’s CPA team can help review and interpret it.

The business owner can confirm the real-world context when needed.

The result is not AI alone.

It is AI plus accounting logic.

AI plus tax awareness.

AI plus CPA judgment.

AI plus owner knowledge.

That is how business owners can get closer to the outcome they actually want:

Less accounting.

More clarity.

Better decisions.

What Business Owners Should Do Next

Business owners should not ignore AI.

But they also should not blindly trust it.

The right approach is practical.

Use AI to reduce repetitive work.

Use AI to organize information.

Use AI to identify patterns.

Use AI to flag issues.

But do not confuse AI output with final financial truth.

Before relying on AI-generated financial information, ask:

Who trained the process?

What accounting logic is being used?

What tax rules are being considered?

Who reviews the output?

What does the owner need to confirm?

Are the books reconciled?

Are the reports tax-ready?

Do the numbers actually help make better decisions?

Those questions matter.

If AI gives you a fast answer but you still do not understand what is happening in your business, you do not have clarity yet.

You have output.

And output is not the goal.

Clarity is the goal.

At EverydayCPA, we help business owners use technology without pretending technology replaces judgment. If you want better financial information without artificial confidence, book a call with Kelly or Cat.

We can help you understand where AI can help, where it needs review, and how to move toward real financial clarity.

FAQ

Can AI categorize business transactions?

Yes. AI can help categorize business transactions by reading transaction data, identifying vendors, recognizing patterns, and suggesting likely categories. But AI categorization should still be reviewed because the same transaction can have different business or tax treatment depending on context.

Is AI bookkeeping accurate?

AI bookkeeping can be useful, but it is not automatically accurate. Its accuracy depends on the quality of the data, the accounting rules used, the business context provided, and whether the results are reviewed by qualified professionals.

Can AI replace a CPA?

AI cannot fully replace a CPA. AI can assist with data processing and pattern recognition, but CPAs provide judgment, tax knowledge, professional review, and business interpretation.

Why is AI alone risky for accounting?

AI alone is risky because it can misclassify transactions, misunderstand deposits, miss tax-sensitive issues, or create reports that look accurate but are not properly reviewed.

What is the difference between AI output and financial clarity?

AI output is information generated by a system. Financial clarity means the information is accurate, reviewed, understood, and useful for tax preparation, cash flow, profitability, and business decisions.

Why can AI misclassify deposits?

AI can misclassify deposits because a deposit may be revenue, loan proceeds, a transfer, an owner contribution, a reimbursement, a refund, or something else. The transaction description alone may not provide enough context.

Why can AI misclassify payments?

AI can misclassify payments because a payment may be deductible, personal, capitalized, reimbursable, loan-related, payroll-related, or subject to special tax treatment. Proper classification often requires context and review.

Does AI need tax rules?

Yes. AI used in accounting and tax should be educated with tax rules, accounting logic, business context, and professional standards. Otherwise, it may produce answers that look useful but are incomplete or wrong.

What role does the business owner play in AI accounting?

The business owner provides context. The owner confirms whether transactions are real, authorized, business-related, unusual, personal, reimbursable, or connected to a specific business purpose.

How does iPacio use AI?

iPacio is designed to use AI to help compile and organize financial activity while EverydayCPA’s CPA team reviews, interprets, and explains the results. The goal is AI-assisted financial clarity, not AI alone.