Kelly Coughlin, CPA

Business Owners Should Not Have to Become Bookkeepers

Business owners do not start companies because they want to reconcile bank statements.

They start companies because they want to sell a product, provide a service, solve a problem, make money, support their family, build something valuable, and create a better future.

But sooner or later, the accounting still has to get done.

That is where many owners get stuck.

The owner knows how to run the business. He knows how to talk to customers. He knows how to sell, deliver, repair, consult, build, design, manage, negotiate, hire, buy, pay, and collect.

That is not usually the problem.

The problem usually begins after the business activity happens.

A transaction occurs. A customer pays. A vendor gets paid. A credit card is used. Money moves between accounts. A contractor gets a check. A subscription renews. A deposit hits the bank. A loan payment is made.

The owner created or authorized the activity.

But then the transaction has to be converted into organized, accurate, tax-ready financial information.

Historically, that has required double-entry accounting, charts of accounts, bank reconciliations, expense categorization, accounting software, bookkeeping rules, tax rules, and a lot of technical knowledge most owners do not have and do not want to learn.

And frankly, they should not have to learn it.

A business owner should understand his business.

He should not have to become the bookkeeper.

That distinction matters.

The owner’s role should be to confirm that transactions are real, authorized, and properly understood in context. The owner should know what happened in the business. But he should not have to personally carry the accounting burden just to get usable financial information.

That is where properly trained AI can help.

But only if the AI is educated by accounting and tax professionals, structured around real business activity, and reviewed by subject matter experts.

AI alone is not enough.

Bookkeeping alone is not enough.

The goal is financial clarity.

Table of Contents

Why Bookkeeping Became the Business Owner’s Burden

The Difference Between Business Activity and Bookkeeping

Step One: The Owner Authorizes the Activity

Step Two: The Accounting Burden Begins

Why Traditional Bookkeeping Feels So Hard

Why QuickBooks Did Not Fully Solve the Problem

The Owner’s Real Role in Financial Information

What the Owner Should Not Have to Do

How AI Can Reduce the Bookkeeping Burden

Why AI Still Needs CPA Review

Tax-Ready Books Require More Than Categorized Transactions

The Better Model: Owner Context + AI Compilation + CPA Judgment

Where iPacio Fits

What Business Owners Should Do Next

FAQ

You should understand your business. You should not have to become the bookkeeper. If your financial system is creating more stress than clarity, let’s talk. Book a Call With Kelly or Cat

Why Bookkeeping Became the Business Owner’s Burden

Most business owners did not choose bookkeeping.

Bookkeeping chose them.

At the beginning, it often feels manageable. There may be one bank account, one credit card, a few customers, a few vendors, and a small number of transactions. The owner can look at the bank account and feel like he has a basic sense of what is happening.

Then the business grows.

More customers. More expenses. More payment platforms. More subscriptions. More contractors. More transfers. More deposits. More credit card activity. More payroll questions. More tax issues.

Suddenly, the owner is expected to understand things he was never trained to do.

What category should this transaction go in?

Is this deposit income, a transfer, a reimbursement, a loan, or an owner contribution?

Is this payment deductible?

Is this expense personal or business?

Should this purchase be expensed or capitalized?

Did the bank feed duplicate this?

Why does QuickBooks show profit if there is no cash?

Why does the balance sheet look strange?

Why does the CPA keep asking questions at tax time?

The owner may be smart, capable, and successful — and still feel completely overwhelmed by bookkeeping.

That does not mean he is bad at business.

It means the accounting system is asking him to do the wrong job.

The Difference Between Business Activity and Bookkeeping

Every business has activity.

The activity is the real-world operation of the company.

A customer pays an invoice. A restaurant buys food. A contractor buys materials. A consultant pays for software. A real estate agent pays for marketing. A designer pays a subcontractor. A store receives merchant deposits. A business owner moves money from checking to savings.

That is business activity.

Bookkeeping is the process of organizing that activity into financial records.

Those are different jobs.

Business activity asks:

What happened?

Bookkeeping asks:

How should it be recorded?

Financial clarity asks:

What does it mean?

Most owners are comfortable with the first question. They know what happened. They were there. They made the sale, paid the bill, bought the equipment, hired the contractor, or approved the credit card charge.

The difficulty comes when they are expected to convert that activity into accounting language.

That is where the burden becomes unreasonable.

The owner should not have to become fluent in accounting just to understand his own business.

Step One: The Owner Authorizes the Activity

Every transaction starts somewhere.

Usually, it starts with the business owner or someone acting on behalf of the business.

The owner sells the product.

Provides the service.

Pays the bill.

Receives the money.

Uses the credit card.

Pays the contractor.

Moves money between accounts.

Approves payroll.

Buys materials.

Pays for software.

Accepts a customer payment.

That is step one: the owner authorizes the activity.

At the most basic level, each transaction usually includes a few facts:

Date

Amount

Payee or payer

Financial institution or payment method

Business purpose

Context

The business owner often knows the context better than anyone.

He knows why the purchase was made. He knows whether the trip was business-related. He knows whether the deposit was a customer payment or a transfer. He knows whether the contractor was hired for client work or internal work. He knows whether the expense was ordinary or unusual.

That knowledge matters.

But knowing the business purpose is not the same as doing the bookkeeping.

The owner creates or authorizes the activity.

That does not mean the owner should be responsible for turning every transaction into tax-ready financial information.

Step Two: The Accounting Burden Begins

After the transaction happens, the accounting work begins.

That is where many owners get frustrated.

The transaction has to be captured, categorized, matched, reconciled, reviewed, and eventually included in reports that support tax preparation and business decisions.

Historically, this has required technical accounting work:

Double-entry accounting

Chart of accounts setup

Bank reconciliations

Credit card reconciliations

Expense categorization

Loan tracking

Owner draw and contribution tracking

Payroll accounting

Revenue classification

Accounts receivable review

Accounts payable review

Tax-sensitive categorization

Documentation review

Financial statement preparation

Most owners do not want to learn all of this.

And they should not have to.

They should understand the results.

They should understand what the numbers mean.

They should be able to make better decisions.

But they should not have to spend their evenings becoming amateur accountants.

The owner’s time is usually better spent selling, managing, delivering, improving operations, serving customers, and building the business.

Why Traditional Bookkeeping Feels So Hard

Traditional bookkeeping feels hard for business owners because it asks them to operate in a system built for accountants.

A chart of accounts does not feel like plain English.

A balance sheet does not always feel intuitive.

Bank reconciliations do not feel like business strategy.

Owner draws, transfers, reimbursements, loans, payroll liabilities, and capital purchases can easily become confusing.

And when the owner does not understand the system, he begins to avoid it.

Avoidance is not laziness.

Avoidance is often a signal that the system is not designed around how owners think.

A business owner may understand the business perfectly well in practical terms. He may know which customers are difficult, which services are profitable, which vendors are essential, which employees are reliable, and which jobs are not worth repeating.

But when all of that activity gets translated into accounting software, it may no longer feel understandable.

That is the problem.

The financial system should help the owner see the business more clearly.

It should not make the owner feel less capable.

Why QuickBooks Did Not Fully Solve the Problem

QuickBooks helped many businesses move away from paper ledgers, manual spreadsheets, and shoebox accounting.

That was a major improvement.

But QuickBooks did not eliminate the accounting burden.

In many cases, it moved the burden onto the owner.

The software can import transactions. But someone still has to know what those transactions mean.

The software can suggest categories. But someone still has to know whether the category is right.

The software can generate reports. But someone still has to know whether the reports are accurate.

The software can reconcile accounts. But someone still has to understand why the reconciliation does not match.

The software can create a profit and loss statement. But someone still has to explain why profit and cash are different.

QuickBooks can be useful.

But QuickBooks does not automatically create financial clarity.

Many owners have QuickBooks and still do not know how the business is doing.

That is not always a software problem.

It is often a process problem.

It is a visibility problem.

It is a financial clarity problem.

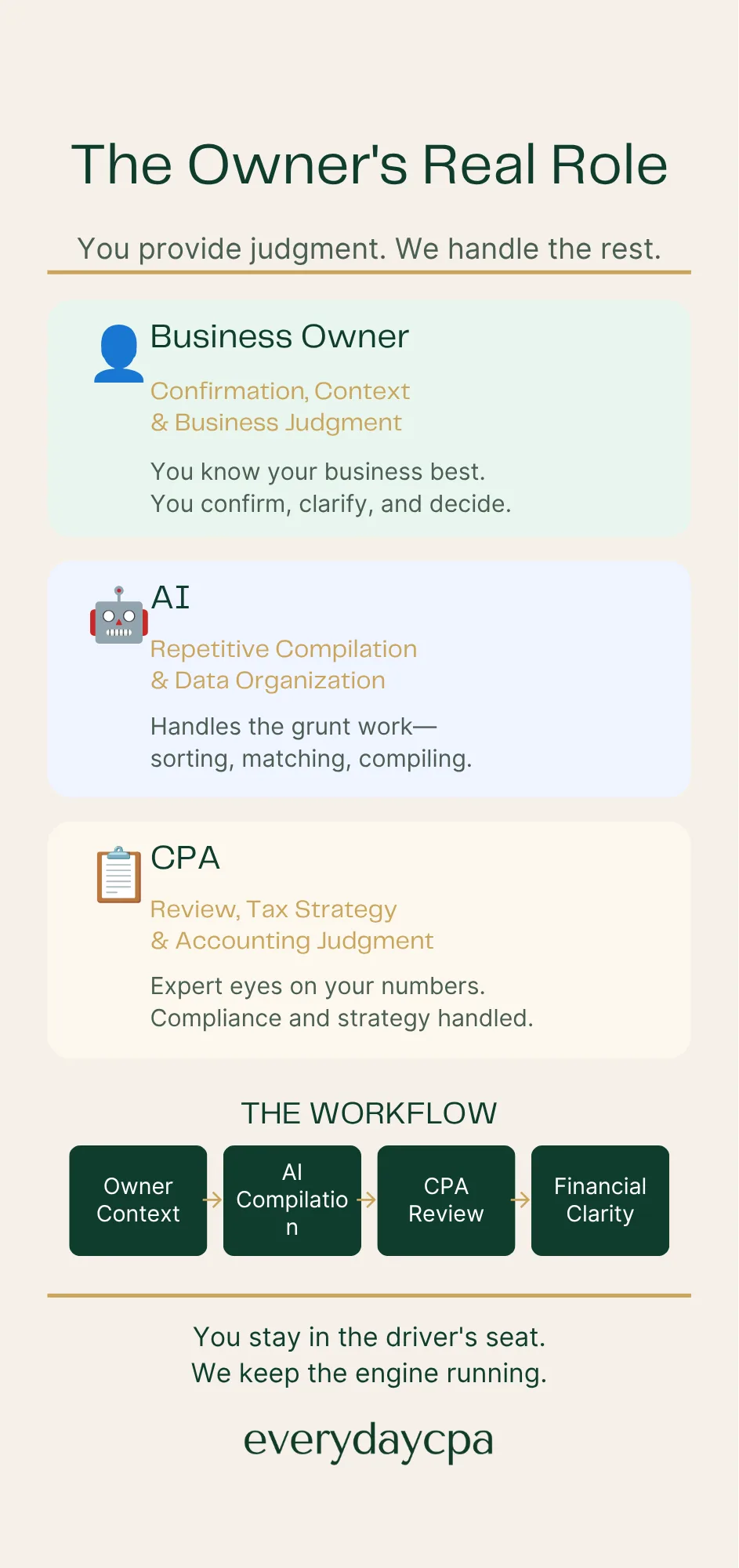

The Owner’s Real Role in Financial Information

The business owner still has an important role.

The owner should not disappear from the process.

No AI system, bookkeeper, CPA, or software platform can fully understand the business without owner context.

The owner should help answer practical questions:

Was this transaction authorized?

Was this purchase business-related?

Was this deposit from a customer, a loan, a transfer, or something else?

Was this charge personal or business?

Was this vendor used for client work or internal operations?

Was this unusual transaction legitimate?

Was this expense connected to a specific project, customer, property, or activity?

That is the owner’s role.

Confirmation.

Context.

Business judgment.

But that is different from bookkeeping.

The owner should not have to build the chart of accounts, categorize every transaction, reconcile every account, clean up every duplicate, interpret every report, and prepare tax-ready records alone.

The owner should be involved where his knowledge is valuable.

He should not be buried where his time is wasted.

Want practical tax and financial clarity tips while you think it over? Download Tax Tips & Hacks free. Download the Free Book

What the Owner Should Not Have to Do

Business owners should not have to become bookkeepers to get reliable financial information.

That means the owner should not have to personally carry the full burden of:

Learning double-entry accounting

Maintaining detailed accounting records manually

Guessing at tax categories

Reconciling every account without support

Fixing bank feed errors alone

Sorting through duplicate transactions

Wondering whether transfers were recorded correctly

Trying to understand balance sheet cleanup

Spending hours inside accounting software

Waiting until tax season to discover problems

Guessing whether books are tax-ready

Some owners can handle some of this, especially early in the business.

But for many owners, this is not the best use of time.

More importantly, it may not produce the best result.

A business owner can spend hours doing bookkeeping and still end up with books that are not tax-ready, not accurate, and not useful for decisions.

That is a bad trade.

The point is not to make the owner better at bookkeeping.

The point is to give the owner better financial information.

If your evenings are disappearing into bookkeeping work, the problem may not be your discipline. It may be the system. Book a Financial Clarity Conversation

How AI Can Reduce the Bookkeeping Burden

AI can help because much of the accounting burden involves repetitive information processing.

AI can read data.

Identify patterns.

Suggest categories.

Compare transactions.

Flag unusual activity.

Summarize information.

Find inconsistencies.

Help organize financial records.

That can reduce the burden on the owner.

For example, AI may help identify recurring vendors, separate likely transfers from likely expenses, flag unusual deposits, detect duplicate transactions, group similar expenses, and surface transactions that need owner confirmation.

That kind of assistance can be valuable.

It can help move the business away from owner-managed bookkeeping and toward a more efficient process.

But there is an important warning.

AI can help compile information.

AI should not be treated as the final judge.

A transaction is not correct just because AI categorized it.

A report is not tax-ready just because AI produced it.

A dashboard is not clarity just because it looks clean.

AI can reduce the burden.

It cannot eliminate the need for judgment.

Why AI Still Needs CPA Review

Accounting and tax require context.

That is why AI still needs CPA review.

A deposit may look like revenue, but it may actually be a loan, transfer, reimbursement, owner contribution, refund, or balance sheet item.

A payment may look like an ordinary expense, but it may need to be capitalized, treated as personal, allocated to a project, reviewed for documentation, or handled differently for tax purposes.

A clean-looking profit and loss report may still hide problems.

Transfers may be misclassified as income.

Personal expenses may be mixed into business activity.

Owner draws may be treated incorrectly.

Loan payments may be recorded as expenses.

Contractor payments may need 1099 review.

Payroll entries may not match payroll reports.

Credit card payments may be double-counted.

AI can miss these issues if it is not trained, supervised, and reviewed.

That is why the best model is not AI alone.

It is AI plus accounting logic.

AI plus tax knowledge.

AI plus CPA judgment.

AI plus owner context.

That combination can produce something far more useful than traditional DIY bookkeeping.

AI can help with the heavy lifting, but your financial information still needs judgment. EverydayCPA combines technology with CPA review. Talk With Kelly or Cat

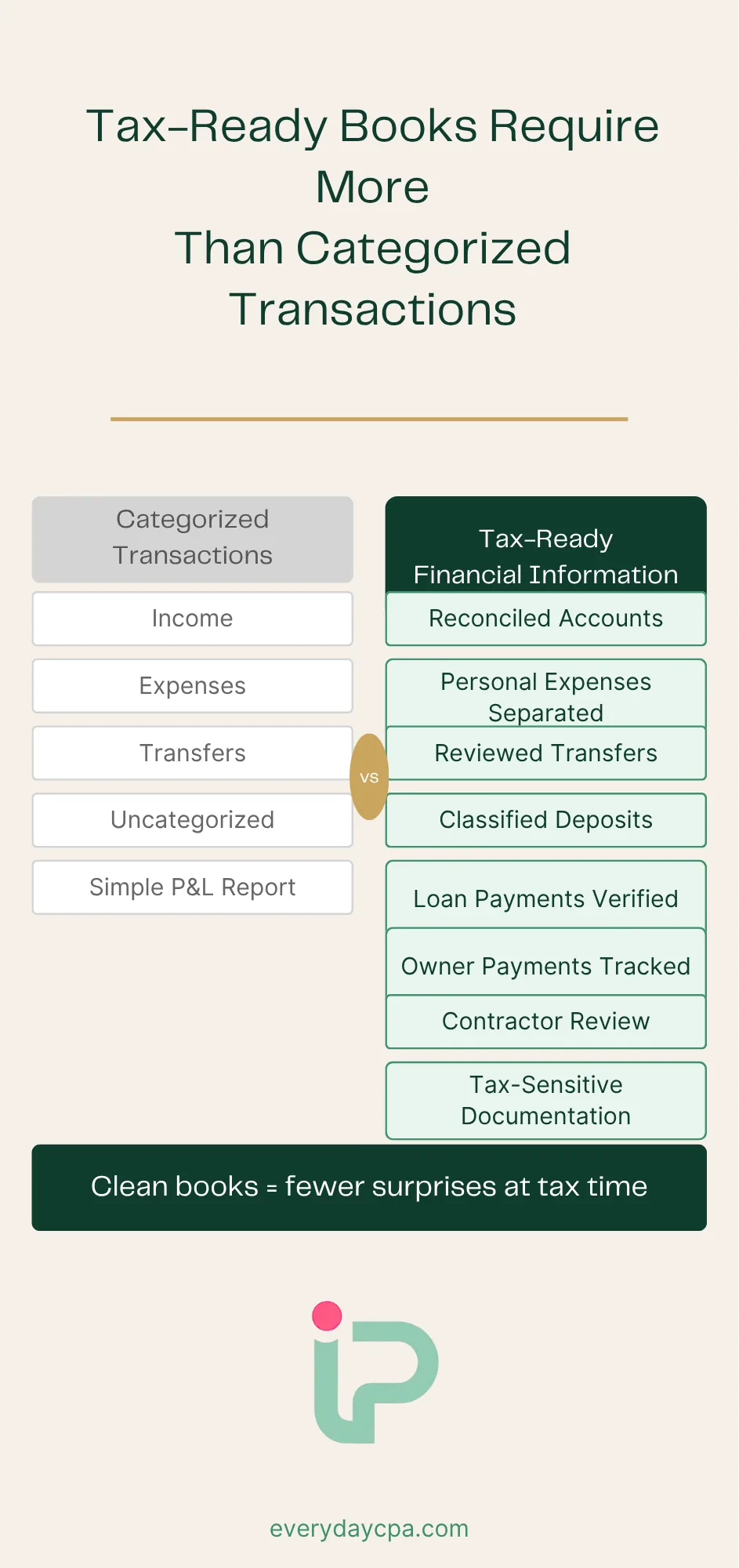

Tax-Ready Books Require More Than Categorized Transactions

A common mistake is assuming that categorized transactions are the same as tax-ready books.

They are not.

Tax-ready financial information requires more than putting expenses into buckets.

The books need to be complete, reconciled, reviewed, and understood through a tax lens.

That means asking questions like:

Are all business accounts included?

Are all credit cards included?

Are personal and business expenses separated?

Are transfers properly excluded from income and expenses?

Are deposits correctly identified?

Are loan payments treated correctly?

Are owner payments classified properly?

Are expenses categorized consistently?

Are contractor payments reviewed?

Are large purchases handled correctly?

Are tax-sensitive items documented?

Are the reports reasonable?

This is where CPA review matters.

The goal is not merely to create books that look organized.

The goal is to create financial information that helps prepare tax returns, manage cash flow, understand profitability, and make better decisions.

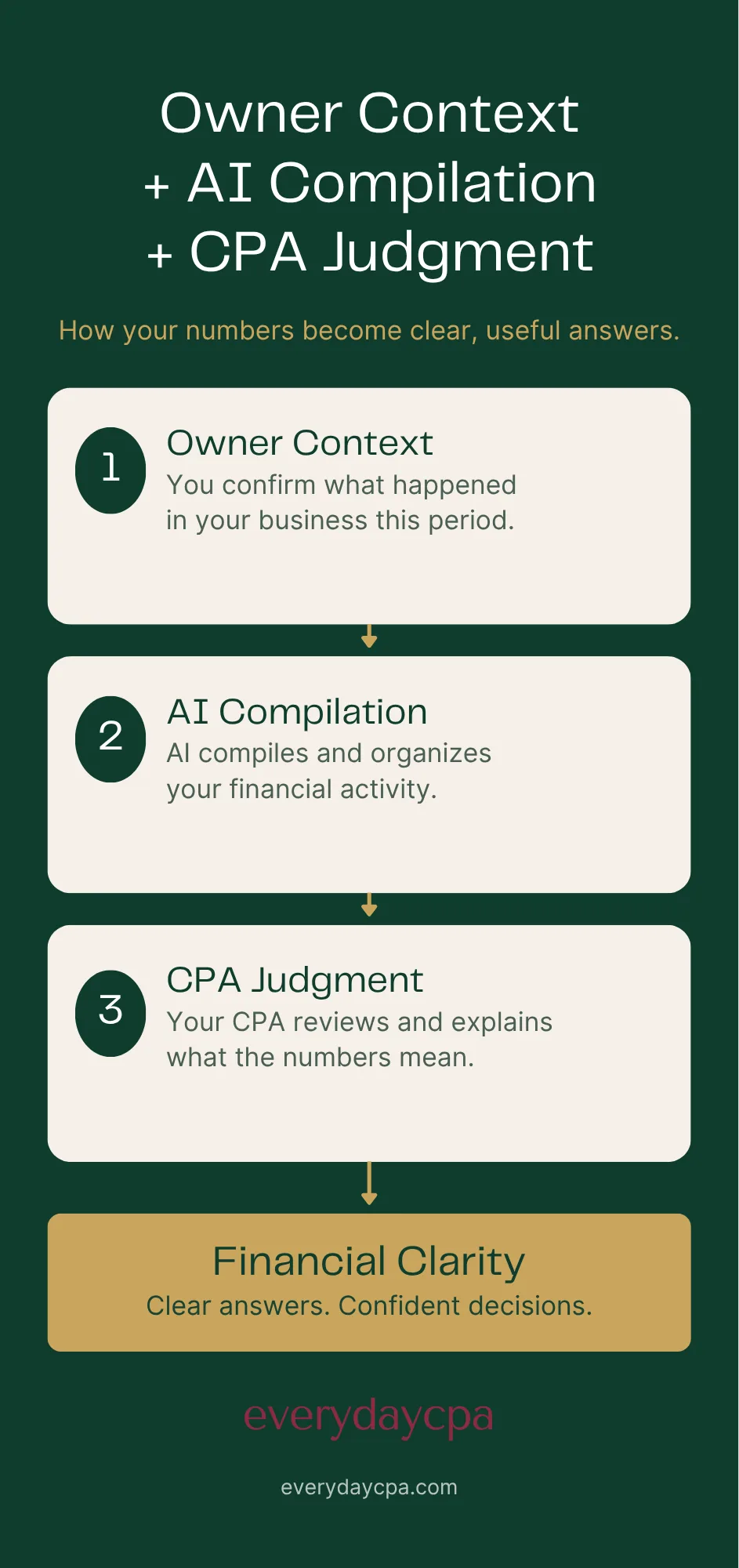

The Better Model: Owner Context + AI Compilation + CPA Judgment

The future should not require business owners to do all their own bookkeeping.

It should also not rely on AI acting alone without professional review.

The better model is a division of labor.

The owner creates and authorizes business activity.

AI helps compile, organize, and flag the financial information.

Accounting and tax professionals train the system, review the results, and apply judgment.

The owner confirms context when needed.

The CPA explains what the information means.

This is a better model because each party does the work it is best suited to do.

The business owner runs the business.

AI handles repetitive compilation work.

The CPA provides tax and accounting judgment.

The owner provides real-world context.

The final output is not just bookkeeping.

The final output is clarity.

This is the shift business owners need.

Less time trying to become bookkeepers.

More time understanding the business.

Where iPacio Fits

iPacio is designed around a simple belief:

Business owners should not have to become bookkeepers to get financial clarity.

The owner still matters.

The owner’s knowledge of the business is essential. But that knowledge should be used where it adds value: confirming transactions, identifying unusual activity, explaining business purpose, and making decisions.

The owner should not have to spend hours managing accounting software just to find out what happened.

iPacio is built to reduce the accounting burden on business owners while keeping CPA review and business judgment in the process.

AI can help compile the activity.

EverydayCPA can help review and interpret the results.

The owner can focus on running the business.

The goal is not to remove people from the process.

The goal is to put the right people in the right roles.

AI helps with the heavy lifting.

CPAs help with judgment.

Owners help with context.

Together, that can create better financial information faster, with less stress and less accounting work for the owner.

iPacio is designed to reduce the accounting burden on business owners while keeping CPA review and business judgment in the process. Learn About iPacio

What Business Owners Should Do Next

The first step is not to feel guilty about bookkeeping.

Many business owners struggle with it because bookkeeping is not what they built the business to do.

The better question is:

Is your current system giving you reliable, tax-ready, decision-ready financial information?

If the answer is yes, keep going.

If the answer is no, the problem may not be that you need to work harder at bookkeeping.

The problem may be that you need a better system.

Ask yourself:

Do I trust my financial reports?

Do I know where the money is going?

Do I know whether the business is profitable?

Do I know what taxes may look like before tax season?

Do I know whether my books are actually tax-ready?

Do I spend too much time trying to fix accounting software?

Do I avoid looking at the numbers because they feel overwhelming?

If those questions feel familiar, you are not alone.

And you do not have to untangle it alone.

At EverydayCPA, we believe business owners should understand their numbers without becoming accountants or bookkeepers. That is the idea behind iPacio.

If you want better financial information with less accounting burden, book a call with Kelly or Cat.

We can help you think through what your current system is doing, where it is breaking down, and how to move toward financial clarity.

FAQ

Should business owners do their own bookkeeping?

Some business owners can manage their own bookkeeping when the business is simple, transactions are minimal, and they understand the process. But as the business grows, bookkeeping often becomes too time-consuming, too technical, or too important to handle without support.

Why is bookkeeping hard for business owners?

Bookkeeping is hard because it requires accounting knowledge, consistent processes, accurate categorization, reconciliations, tax awareness, and software management. Most business owners were trained to run their business, not to perform accounting work.

What is the business owner’s role in bookkeeping?

The business owner’s most important role is to provide context. The owner should confirm that transactions are real, authorized, and properly understood. The owner should not necessarily have to categorize every transaction, reconcile every account, or prepare tax-ready books alone.

Can AI do bookkeeping for business owners?

AI can assist with bookkeeping by reading transaction data, identifying patterns, suggesting categories, and flagging unusual activity. But AI bookkeeping still needs accounting logic, tax knowledge, CPA review, and business owner context.

Can AI replace a bookkeeper?

AI can reduce some bookkeeping tasks, but it should not be treated as a full replacement for trained review. AI can make guesses, but tax-ready financial information requires judgment, context, and oversight.

Why is AI alone not enough for accounting?

AI alone is not enough because accounting and tax require judgment. AI may not know whether a transaction is revenue, a transfer, a loan, a reimbursement, deductible, personal, capitalized, or misclassified. Expert review is still needed.

What does tax-ready bookkeeping mean?

Tax-ready bookkeeping means financial information is organized, complete, reconciled, reviewed, and prepared in a way that can support tax return preparation and tax planning. It requires more than simply categorizing transactions.

What is financial clarity?

Financial clarity means understanding what is happening in the business well enough to make confident decisions. It includes visibility into cash flow, profitability, expenses, taxes, and risks.

How does iPacio help business owners?

iPacio is designed to reduce the accounting burden on business owners by using AI-assisted compilation, CPA review, and owner context to create clearer financial information and better decision support.

Do I still need a CPA if I use AI bookkeeping?

Yes, for many businesses. AI can help organize information, but a CPA can review the results, identify tax issues, apply judgment, and explain what the numbers mean for the business.

You do not need to become a bookkeeper to run a successful business. You need better financial clarity. Book a Call With Kelly or Cat